Kolkata | April 2026

West Bengal is rapidly emerging as a key driver of India’s microfinance growth story, with borrowers increasingly moving toward formal credit systems and using loans for income-generating activities, according to a joint study by Microfinance Industry Network (MFIN) and National Council of Applied Economic Research (NCAER).

The report highlights a significant behavioural shift among borrowers in the state, with a growing preference for regulated lenders over informal sources. This transition is helping strengthen household incomes, improve savings habits, and enhance overall financial stability.

Key Findings

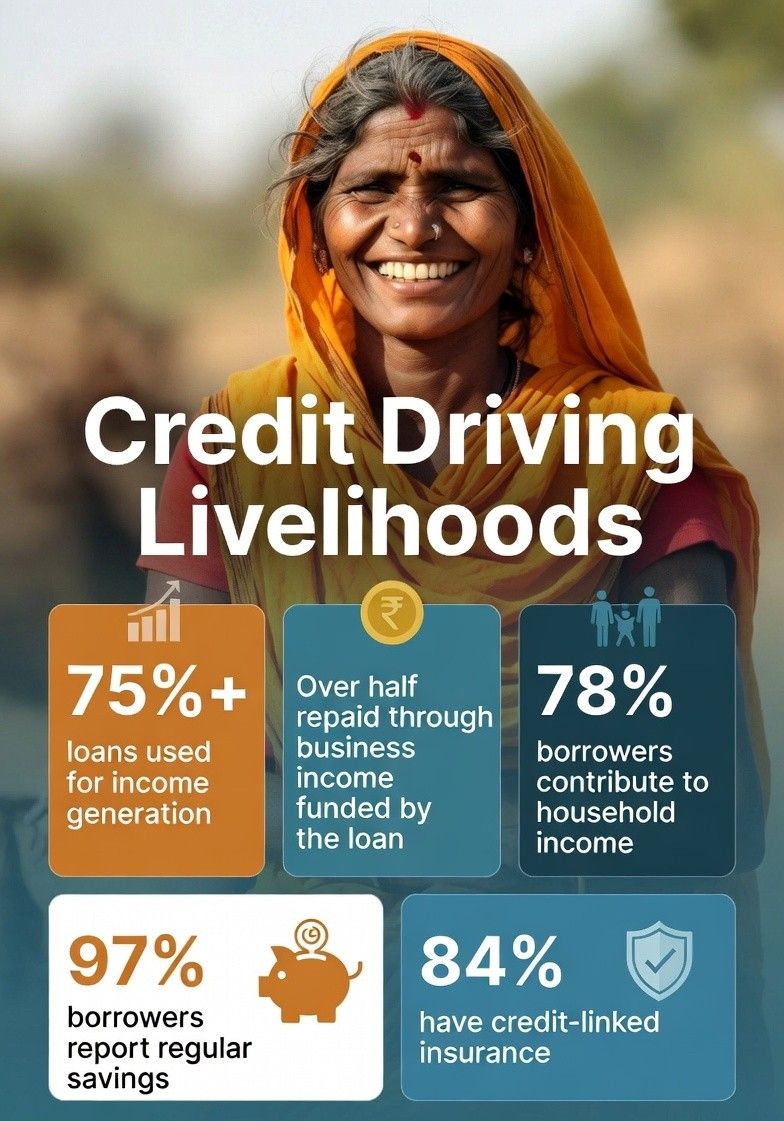

- 78% of borrowers in West Bengal contribute to household income, underlining the strong economic participation of women borrowers.

- The average annual household income stands at ₹3.14 lakh, reflecting steady financial progress.

- The state records the highest share (46%) of borrowers engaged in petty trade and small businesses, indicating a strong linkage between credit and livelihoods.

- Borrowers are increasingly using loans for productive purposes such as business expansion, new enterprises, and farm-related activities rather than consumption.

- Non-food consumption expenditure in the state is higher than the national average, pointing to improved living standards.

Driving Financial Inclusion

The study underscores that microfinance in West Bengal is no longer just a credit tool but a catalyst for economic empowerment. Regulated institutions are gaining trust due to their accessibility, transparent processes, and support in managing household cash flows.

Dr. Alok Misra noted that the sector is witnessing a “clear shift towards formal credit,” along with reduced dependence on informal lending. However, he emphasized the need for stronger credit assessments to prevent over-indebtedness and ensure sustainable growth.

Meanwhile, V. Anantha Nageswaran highlighted the broader opportunity, stating that strong borrower relationships can now be leveraged beyond credit—through financial literacy, skill development, and income enhancement initiatives.

The Big Picture

West Bengal stands out as a model for how small, regulated loans can transform livelihoods. With rising financial awareness and responsible lending practices, the state is paving the way for deeper financial inclusion and long-term economic resilience.

Bottom Line:

From informal borrowing to structured finance, West Bengal’s microfinance landscape is evolving—fueling entrepreneurship, empowering households, and strengthening the foundation of inclusive growth.